OPEC+ deal too little, too much, then just right for OPEC’s expected oil market

OPEC+ deal too little, too much, then just right for OPEC’s expected oil market

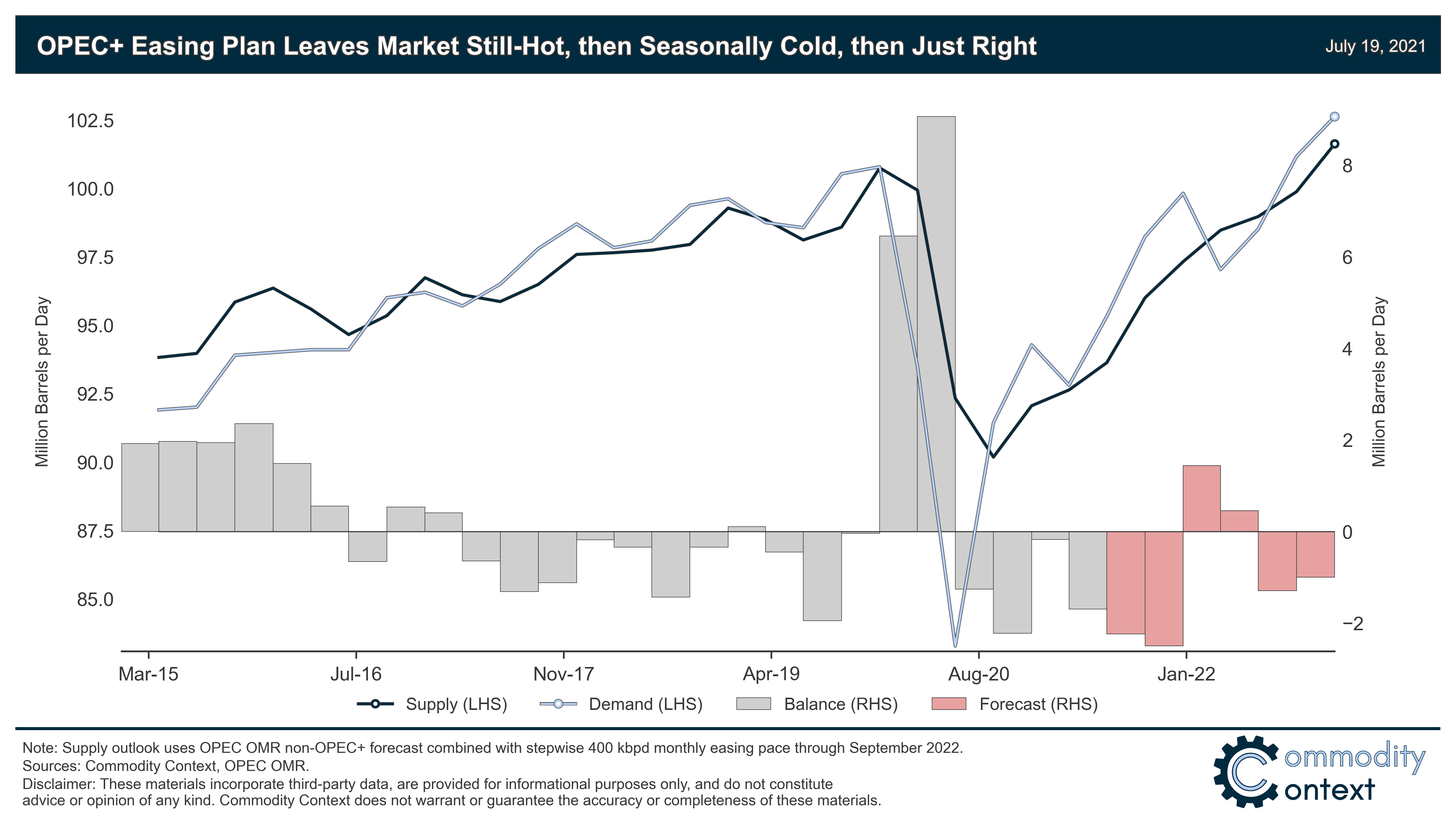

OPEC expects oil market to continue tightening but face seasonal demand speedbump in the first half of next year

OPEC+ finally agreed to extend its output deal through end-2022 and lift production by 400 kbpd per month until the original 9.7 MMbpd cut has fallen off entirely (Fall 2022).

Despite this production boost, oil balances are expected to remain very tight in the latter half of 2021 and the market could have readily absorbed a more aggressive easing rate through year-end.

But then OPEC’s own forecasting calls for seasonal demand weakness in the first half of 2022 that would flip the market back into surplus for the first time since the beginning of the pandemic, before tightening again through the end of next year.

The baseline bruhaha seemingly benefitted five baseline-revised members, but generally will be a more-heat-than-light development for markets at the end of the day.

At long last, OPEC+ members have finally agreed to extend their existing deal through the end of 2022. This agreement will see members increase their collective production target at a steady, stepwise pace of 400 thousand barrels per day (kbpd) each month from August 2021 through Fall 2022, at which point the full 9.7 MMbpd of original cuts will have fallen off entirely. The baseline bruhaha, which caused the initial stand-off and subsequent negotiation postponement, won’t become relevant until May 2022—if at all—and those adjustments are discussed in all their fuzzy glory more fully below.

The OPEC+ compromise and steady easing pace is good news for the oil market, as I stated in my last newsletter. The oil market desperately needs additional barrels to ease current artificial tightness. Indeed, the market likely could have absorbed 1-2 MMbpd more crude by year-end than was secured in this deal, with balances in the second half of 2021 (2H21) likely remaining in a deficit of millions of barrels per day. Therefore, even with this boosted OPEC+ production path, tight spot market conditions will likely contribute to further upward price pressure over the coming months.

But then OPEC’s own forecasts begin to paint a weaker demand picture in the first half of 2022, which when combined with still-rising OPEC+ output flips the market into surplus for the first time since the initial May 2020 cut to offset the pandemic demand rout. Given the amount of speculative money still supporting the price of crude, even a temporary return to oversupply, contango, and rising inventories could prompt a harsh—though transient—rout.

Things start to look more durably bullish going into the second half of 2022 when OPEC+ cuts have rolled off and the market is facing tighter conditions with what are by then low global crude inventories and slim OPEC spare capacity. The handoff into 2023 is setting up to be especially tight absent renewed growth from non-OPEC+ producers (e.g. the newly growth averse US shale patch) or a moderation of post-pandemic demand gains.

Tranquility Baseline. The Eagle has landed—kinda

While the agreement was explicit about the easing pace and extension timeline, the more controversial baseline adjustments were left diplomatically fuzzy and ultimately lack any immediate market impact.

The UAE got some of what it was after: its baseline will be increased by roughly 350 kbpd to 3.5 MMbpd, which is better than the initial October 2018 baseline but only half-way to the 3.84 MMbpd produced in April 2020. Good luck changing only one country’s baseline, though. Four other members used this opportunity to extract their own concessions: Saudi Arabia and Russia each added 500 kbpd to their baselines, and Iraq and Kuwait each got a boost of 150 kbpd. In total, the group’s collective baseline will rise by more than 1.6 MMbpd on May 1st, 2022.

Ultimately, this baseline hike is likely more for show than any real trigger for growth. Roughly two-thirds of the overall baseline increase went to Saudi Arabia—which has typically over-complied with cut requirements—and Russia—which despite steady quota cheating faces a host of operational challenges to ever reaching this higher production quota. Even for the lucky members that received baseline upgrades and would produce more if they could, the general understanding of the deal is that the 400 kbpd easing pace would be unaffected by these baseline revisions. The main benefit these five baseline-revised members will receive is a greater proportional share of the 400 kbpd easing pace from May 1, 2022 forward.

Even the endpoint of the cuts will remain unchanged: a further 5.8 MMbpd of easing from July allowances and a total rollback of the 9.7 MMbpd of cuts from October 2018 levels. The implicit spare capacity that remains in countries like the UAE seems to have been left as a topic for another day. All in all, the baseline discussion consumed way, way more oxygen (and my attention) than it deserved and appear to be a true more-heat-than-light kerfuffle in classic OPEC tradition.

In the end, OPEC+’s production deal came in broadly as expected and when contextualized with OPEC’s latest 2021-22 forecasts yields a steadily tighter oil market only temporarily derailed by a seasonal demand slump in the first half of 2022 before tightening again as we head into 2023.